We live in an era where medical technology has reached incredible heights, but so has the cost of treatment. Today, a single week in a premium hospital for a major ailment can cost more than a luxury international vacation. For most middle-class families, a medical emergency is not just a health crisis; it is a financial disaster that can wipe out years of hard-earned savings.

This is where Health Insurance steps in. It is not just a policy; it is a financial shield that ensures you get the best medical care without worrying about the bill. In this ultimate guide, we will explore how you can save lakhs on medical bills by choosing the right Health Insurance plan.

1. The Rising Cost of Healthcare in India

Medical inflation in India is rising at a staggering rate of 12-14% annually. Procedures that cost ₹2 Lakh five years ago now cost upwards of ₹4 Lakh. Whether it is a planned surgery or an emergency hospitalization, the “room rent,” “doctor’s fees,” and “diagnostic tests” add up to a mountain of debt.

By investing in Health Insurance, you transfer this financial risk to the insurance company. For a small annual premium, you secure a cover of ₹5 Lakh, ₹10 Lakh, or even ₹1 Crore, ensuring that a hospital visit doesn’t become a debt trap.

2. Types of Health Insurance: Which One Do You Need?

Not all policies are created equal. To save the most money, you must choose a plan that fits your family’s needs:

- Individual Health Insurance: Best for single adults or those with specific health risks.

- Family Floater Plans: One policy covers the entire family (spouse and children). It is usually cheaper than buying separate policies for everyone.

- Senior Citizen Plans: Specially designed for parents aged 60+, covering age-related ailments and pre-existing diseases.

- Critical Illness Cover: A fixed-benefit plan that pays a lump sum amount if you are diagnosed with a life-threatening disease like Cancer or Heart Attack.

3. The Magic of “Cashless Hospitalization”

One of the biggest advantages of modern Health Insurance is the Cashless Claim facility. When you get treated at a “Network Hospital,” you don’t have to pay the bill from your pocket.

- How it works: You show your insurance card at the hospital desk, the insurer approves the treatment, and they settle the bill directly with the hospital.

- The Benefit: You don’t have to break your Fixed Deposits (FDs) or sell gold during an emergency. Your liquidity remains intact.

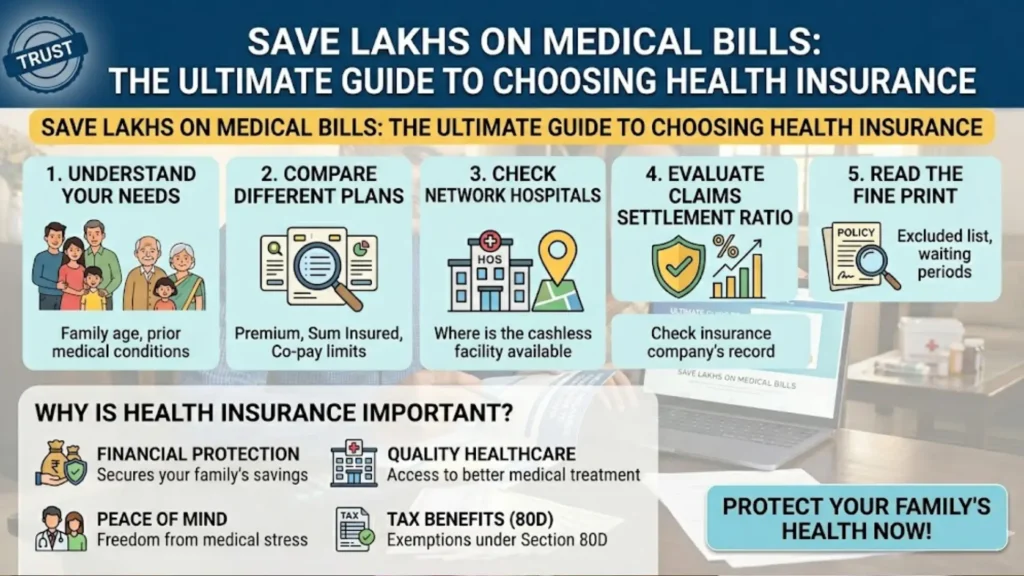

4. Key Factors to Check Before Buying

To ensure you are truly protected and won’t face surprises during a claim, look for these 4 pillars of a good policy:

A. No Room Rent Sub-limits

Many cheap policies have a “sub-limit” on room rent (e.g., 1% of the sum insured). If your room exceeds this limit, the company proportionally reduces your entire bill payout! Always choose a policy with No Room Rent Sub-limits.

B. Waiting Period for Pre-existing Diseases (PED)

If you have Diabetes or BP, the policy won’t cover them from day one. Look for a plan with a Short Waiting Period (usually 2 to 3 years) so that you are covered for your existing conditions as soon as possible.

C. Restoration Benefit

What happens if you use up your entire ₹5 Lakh cover in one surgery? Restoration Benefit automatically refills your sum insured for the next illness within the same year at no extra cost. This is a lifesaver for families.

D. Day Care Procedures

Modern medicine allows many surgeries (like Cataract or Dialysis) to be done in less than 24 hours. Ensure your Health Insurance covers Day Care Procedures so that you aren’t denied a claim just because you weren’t “admitted overnight.”

5. Saving on Taxes: The Double Benefit

While Health Insurance saves you from hospital bills, it also saves you money every year through taxes. Under Section 80D of the Income Tax Act:

- You can claim a deduction of up to ₹25,000 for yourself, spouse, and children.

- You can claim an additional ₹50,000 if you are paying for your senior citizen parents. Total tax-saving potential can be up to ₹75,000, which effectively makes your insurance premium much cheaper.

6. Why “Corporate Insurance” is Often Not Enough

Many people rely solely on the health cover provided by their employer. While it is a great perk, it has major flaws:

- Job Dependence: If you lose your job or switch companies, you are uninsured during the transition.

- Low Cover: Corporate plans usually have a small limit (₹2-3 Lakh), which is insufficient for major surgeries.

- No Customization: You cannot add specific riders like Maternity Cover or OPD Cover to a corporate plan. Pro Tip: Always have a personal Health Insurance policy as a primary backup.

7. The Concept of No Claim Bonus (NCB)

If you stay healthy and don’t make a claim, your insurance company rewards you. Most companies increase your Sum Insured by 10% to 50% every year without charging extra premium. Over 5 years, your ₹5 Lakh cover can grow to ₹10 Lakh for free! This is one of the best ways to increase your protection without increasing your costs.

8. Annual Health Checkups: Prevention is Cheaper

Most premium Health Insurance plans offer a Free Annual Health Checkup. By utilizing this, you can detect potential health issues early. Early detection leads to cheaper and faster treatment, ultimately saving you from massive future hospitalizations.

9. Conclusion: Don’t Wait for a Crisis

Health Insurance is the only thing you can’t buy when you need it the most. Buying it when you are young and healthy ensures lower premiums and a “waiting period” that finishes while you are still fit.

By choosing a policy with No Sub-limits, Restoration Benefits, and a wide Network of Hospitals, you are not just buying a piece of paper; you are buying a guarantee that your family’s future and finances will always remain secure.

Save your lakhs, secure your life, and invest in a Comprehensive Health Insurance plan today!